Ecommerce

Payment Gateways for Ecommerce: A Guide for Georgia Merchants

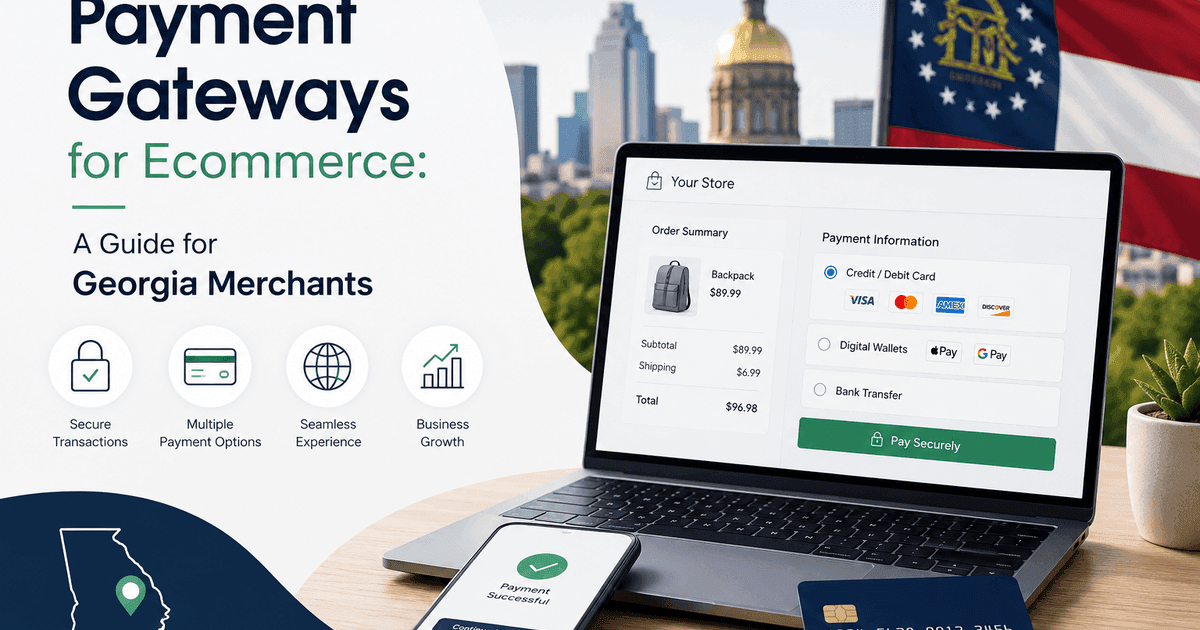

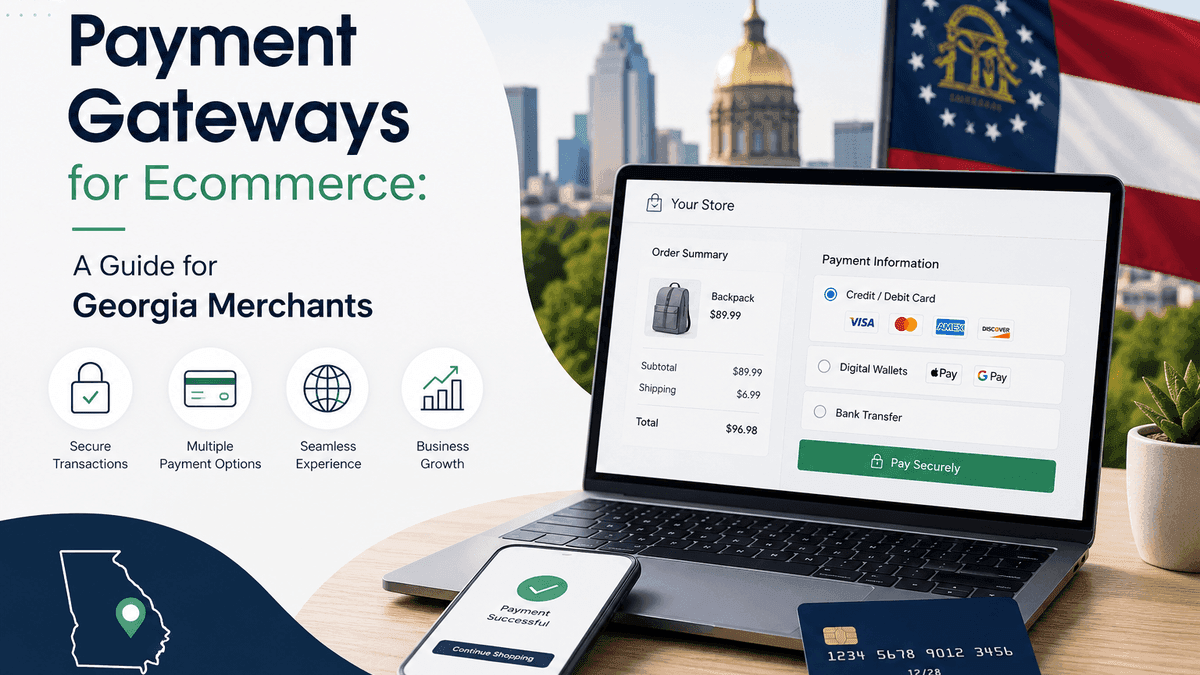

Your ecommerce gateway is the front door for card data online. Georgia merchants selling statewide or nationwide need gateways that balance PCI scope, cart integrations, and honest processing—not just the lowest per-transaction quote.

Gateway roles in plain language

A gateway authorizes and captures online payments, connects to your shopping cart or invoicing tool, and tokenizes card data so it does not live on your server. Hosted payment pages shrink PCI scope; direct API integrations offer more control with more security responsibility.

What to compare beyond price

Cart plugins, recurring billing, level 2/3 fields for B2B, fraud filters, and deposit timing all matter. A cheap gateway that fights your platform every Black Friday costs more than a slightly higher per-txn fee with stable uptime.

- Confirm plugin support for Shopify, WooCommerce, or your custom stack.

- Use AVS, CVV, and velocity rules on card-not-present orders.

- Match descriptor text to your store name customers recognize.

PCI and SAQ type for online sellers

Fully outsourced checkout often qualifies for shorter SAQs; custom cart integrations may not. Revisit SAQ choice when you add subscriptions or store cards on file. See our PCI overview articles and gateway list at /gateways for starting points.

Pair the right gateway with transparent processing

Omega Bank Card helps Georgia ecommerce merchants compare gateways at /gateways and attach interchange-plus pricing at /interchange-plus so online volume is auditable like in-store taps. Bring your cart URL and last month’s processing—we will map a stack that fits how you sell, not a generic plugin bundle.

POS and processing are one system—price them together

Hardware quotes are easy to compare; total cost of ownership is not. Software modules, per-device fees, gateway add-ons, and processing markup interact on the same deposit. A "free" terminal with opaque tiered processing can cost more than purchased equipment on interchange-plus within a year.

Tour POS options—Clover, Retailz, Union, and others—with your statement in hand. Clover for Atlanta restaurants and Retailz for convenience retail show how vertical workflows change device choice.

Omega Bank Card pairs equipment decisions with interchange-plus pricing so savings from better capture habits show on the statement—not just in shorter lines.

Deployment details that prevent day-one friction

Order numbers, MID activation, tipping presets, tax lines, offline mode, and gateway credentials should be tested on live small transactions before you open the doors. Underwriting approval without configured terminals is a common opening-week failure mode for new Atlanta locations.

Virtual terminals and physical terminals carry different PCI scopes. Virtual vs physical terminals and SAQ selection should be reviewed whenever you add phone orders or ecommerce.

For ecommerce-heavy stacks, compare payment gateways on plugin support, fraud tools, and deposit timing—not just per-transaction price.

- Standardize devices and closeout routines before opening location two.

- Label each terminal in reporting so downgrades trace to a store.

- Confirm tip adjust and pre-auth flows match your service model.

- Keep processor support contacts visible at the manager station.

Scale hardware without scaling confusion

Multi-unit operators should decide reporting hierarchy before adding handhelds or kiosks. MID strategy affects how chargebacks, reserves, and tax reporting flow to headquarters.

Read POS guide and equipment guide and underwriting timelines if you are adding locations or new tender types. Request a demo or quote when you are ready to align POS and processing with how guests actually pay in 2026.

Common questions merchants ask about this topic

Merchants researching "Payment Gateways for Ecommerce: A Guide for Georgia Merchants" usually want three answers: what will I actually pay after fees, what changes at the register, and what happens if something goes wrong with a chargeback or compliance notice. Those answers live on your statement and in your terminal settings—not in a generic rate quote.

Omega Bank Card recommends a quarterly fifteen-minute review: effective rate trend, new line items, batch closeout discipline, and whether your PCI attestation is current. Small fixes often beat processor churn. When churn does make sense, move with statement math and a documented migration checklist so deposits do not gap during the switch.

Still comparing options? Browse more articles on the Omega blog, explore credit card processing services, or request a free statement audit to ground the conversation in your real numbers.

- How do I calculate effective rate? Total fees ÷ card sales for the same period.

- When should I switch processors? When transparency or service blocks fixes—or savings clear your switching cost hurdle.

- Does Omega support my industry? We serve retail, restaurants, healthcare-adjacent, field service, ecommerce, and high-risk verticals with sponsor-bank fit reviewed up front.

- Where do I start? Get started or fee check with a recent PDF statement.

A sustainable review rhythm keeps costs predictable

One-time processor shopping fixes yesterday’s rate—not next quarter’s card mix. Set a recurring calendar reminder to export your statement PDF, recalculate effective rate, and note any new line items. Hidden fees often appear after promotional periods end, equipment leases begin, or PCI non-compliance triggers monthly penalties.

Pair financial review with operational review: Are managers batching terminals on schedule? Is keyed entry limited to true phone orders? Are ecommerce descriptors recognizable? Those habits affect ecommerce businesses as much as basis-point negotiations—especially when rewards cards dominate weekend volume.

Omega Bank Card serves Atlanta-area merchants and businesses nationwide. Whether you need gateways for online sales, wireless terminals for field teams, or high-risk underwriting reviewed up front, anchor decisions in statement math—not slogans. Get started when you want a partner who documents recommendations in writing.

- Compare this month’s effective rate to the same month last year—not only to last month.

- Archive processor change letters; they explain new fees months later.

- Train seasonal staff on EMV and tap before peaks, not during them.

- Keep related blog guides bookmarked for your finance lead and floor manager.

Put the checklist to work this week

Knowledge only helps when it changes a habit or a contract term. Block thirty minutes with your manager or bookkeeper: pull last month’s statement, mark any line you cannot explain, and list checkout scenarios that still rely on keyed entry. That short exercise usually surfaces more savings than another round of generic rate quotes.

If this article overlaps with companion guide and follow-up read, read both before you call your processor—armed questions get clearer answers. Omega’s free statement audit is built for that conversation: we translate dense PDFs into decisions you can make without a payments engineering degree.

When you are ready to compare structured options—not just swap one teaser rate for another—contact Omega Bank Card. We will map payment gateways for ecommerce: a guide for georgia merchants to the processing model, hardware, and compliance posture you actually run today.

Comments

Loading comments…

Related reads

Equipment

Virtual Terminal vs. Physical Terminal: Which Fits Your Workflow?

Virtual terminal vs countertop terminal: pricing differences, PCI implications, card-present vs card-not-present risk, and best uses for each.

Compliance basics

PCI SAQ Types: Which Questionnaire Does Your Business Need?

PCI SAQ types explained for merchants: SAQ A, B, B-IP, C, D, and how your checkout setup determines which self-assessment questionnaire applies.

POS strategy

Union POS Guest-Led Ordering: Benefits for Busy Bars and Restaurants

Union POS guest-led ordering: QR tabs, wallet pay, less server wait time, and how phone-first ordering pairs with transparent processing.

Want a second opinion on your statement?

We review what you pay today, line by line, and show how transparent pricing compares-no obligation to switch.

Get a Free Statement Audit